Over the past five years, collateralized loan obligations (CLOs) have delivered some of the best risk-adjusted returns available in fixed income markets.

AA and A rated CLOs bridge the gap between the AAA and BBB segments, providing attractive returns with strong credit ratings and moderately low volatility.

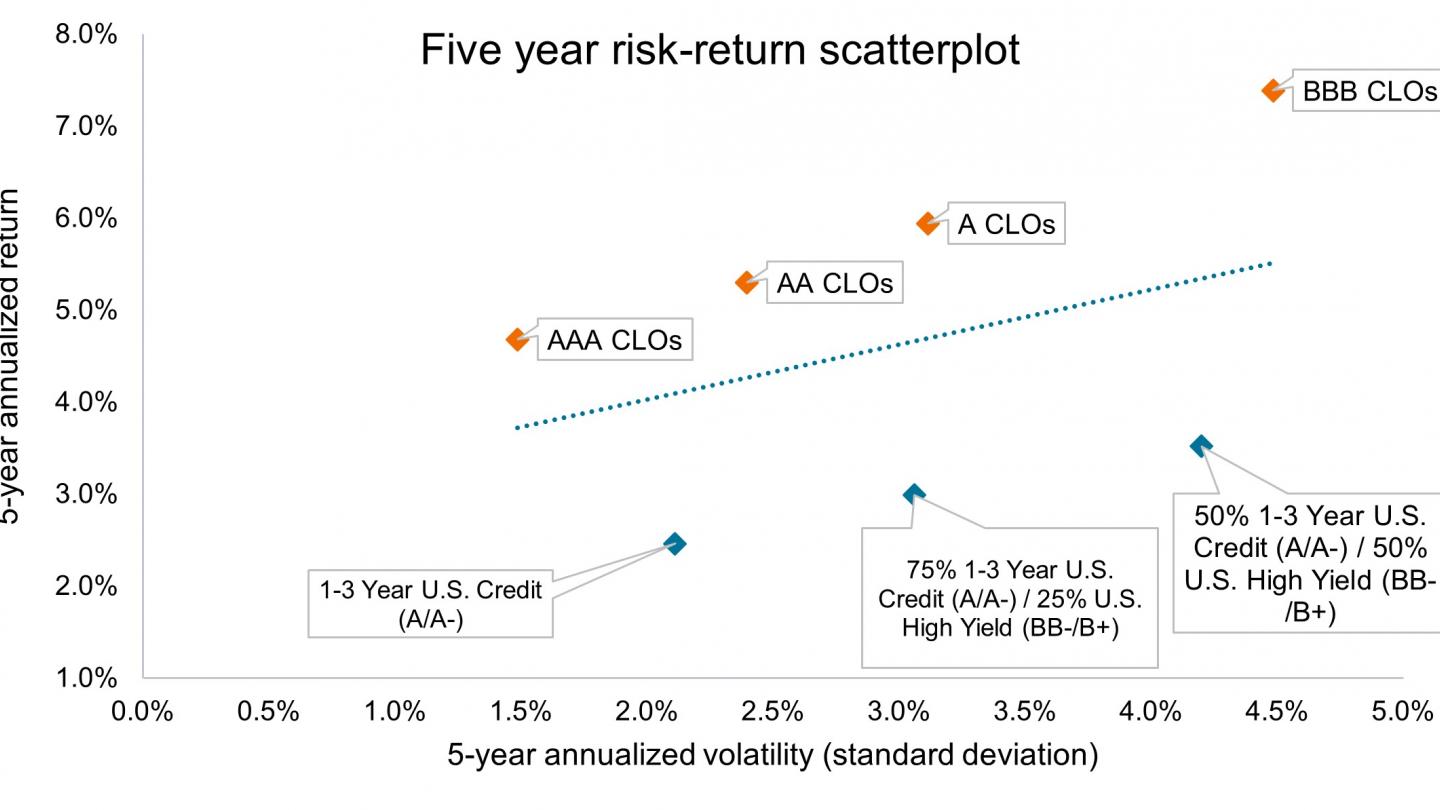

Key takeaways

- In our view, CLOs provide a highly efficient source of yield. For example, A rated CLOs returned 5.9% per year for the five-year period ended 31 December 2025, while a portfolio of 75% 1-3 Year U.S. Credit / 25% U.S. High Yield with virtually the same level of volatility delivered just 3.0% per year.

- For investors prioritizing low volatility, AAA CLOs might be a good option. Those seeking more return with a slightly higher risk profile may consider layering in AA and A CLOs.

- While BBB CLOs may appeal to the more aggressive investor with a higher risk appetite, AA and A tranches remain inherently low volatility due to their minimal interest-rate risk, structural credit enhancements, and strong credit ratings.