Owing to the unprecedented coronavirus pandemic, emerging market (EM) debt, including EM corporate debt, has had a challenging time of late. Indeed, the nearest comparison for the size of declines we saw in March was the 2008 financial crisis period. In recent weeks the market has recovered some of its lost ground, but remains well below pre-‘coronacrisis’ levels. Given all the uncertainties, this is to be expected. However from a long-term 3-5 year view, we think there are grounds for optimism.

Past the worst

Clearly the biggest risk factor at present is the question of when the pandemic will be bought under control. While the rate of progress will inevitably vary across countries, our view is that this will increasingly be achieved in coming months. In recent weeks lockdown measures have begun to be eased in a number of countries. Indeed, it is notable that a number of emerging market countries, such as China and Taiwan, have been among the most successful in this regard.

The (not-so-long) road to recovery…

At the same time, an unprecedented amount of support is coming from world governments and central banks, aimed at limiting the economic damage from the pandemic. While a historically sharp global recession is certain, progressively easing lockdowns, coupled with strong policy support measures, should enable a strong economic recovery in the second half of the year. As such, for many companies, coronavirus will mainly constitute a short-term earnings shock rather than something that endangers their fundamental credit-worthiness. In this respect, the ‘coronacrisis’ is quite different to the last financial crisis, which was routed in far more deep-seated problems, related in part to excessive indebtedness.

Past crisis period perspective

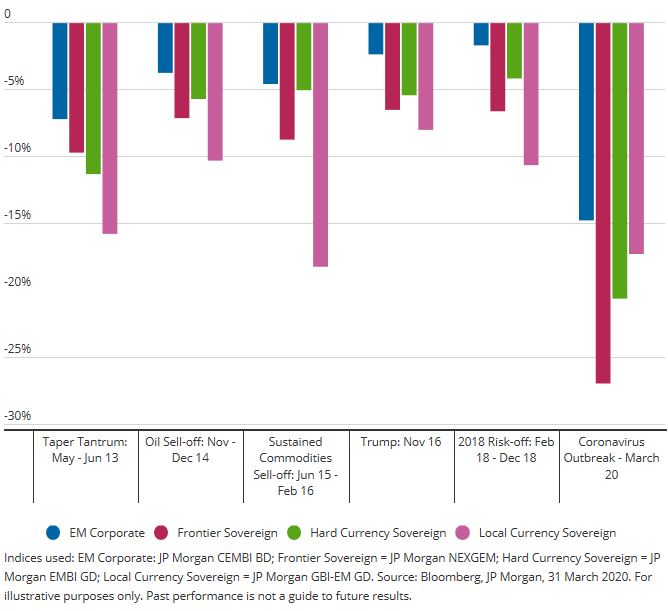

When it comes to EM bonds, it is worth bearing in mind that investors essentially have four alternatives available to them. Namely these are: ‘hard currency sovereign bonds’ – the debt of EM countries in low risk currencies, most commonly US dollars; ‘local currency sovereign bonds’ – the debt of EM countries in their own (typically much more volatile) currencies; frontier market bonds – the debt of typically smaller, less developed countries; and corporate bonds – the debt of EM companies, typically in US dollars. As the chart below shows, when it comes to considering downside risks, EM corporate bonds have a better record of limiting downside risk compared to the three other segments. This was also true in the recent coronavirus-related sell-off.

Relative performance of EMD asset classes through past market downturns

Modest indebtedness

There are lots of reasons that can help to explain the past relative resilience of EM corporate bonds. For example, one key factor is that this type of debt is usually issued in lower risk hard currencies, usually US dollars. Another important factor that can also provide a measure of reassurance is that in the lead up the ‘corona-crisis’, the credit position of EM companies had been on a largely improving trend. For example, net leverage (a key measure of indebtedness) had generally been declining for the past few years. This prudence contrasts quite markedly with some other parts of the global corporate debt world. For example in the case of US investment grade companies, net leverage was recently at 15-year highs.

Active management paramount

Despite the aforementioned positives, there is little doubt that default rates across the whole corporate debt world, including EM corporate debt, will spike significantly from very low levels. Volatility is also likely to remain elevated, with markets remaining particularly sensitive to incoming coronavirus and economic data. As such, we think this really underscores the potential value of active management that is both responsive to new developments and effective at credit selection.

Now more than ever, we think research efforts should focus on finding the corporate bonds of high quality companies with robust balance sheets, sustainable growth models, strong ESG credentials and credible management. Not only should companies like this survive the coronavirus pandemic but rewardingly for their investors, many could well emerge even stronger.

Siddharth Dahiya, Head of Emerging Market Corporate Debt

Aberdeen Standard Investments